According to the National Association of Realtors, the average monthly mortgage (based on average 30-year mortgage rates and home prices) rose 85% in the past 20 months, from $1,212 in January 2022 to $2,243 in August 2023.

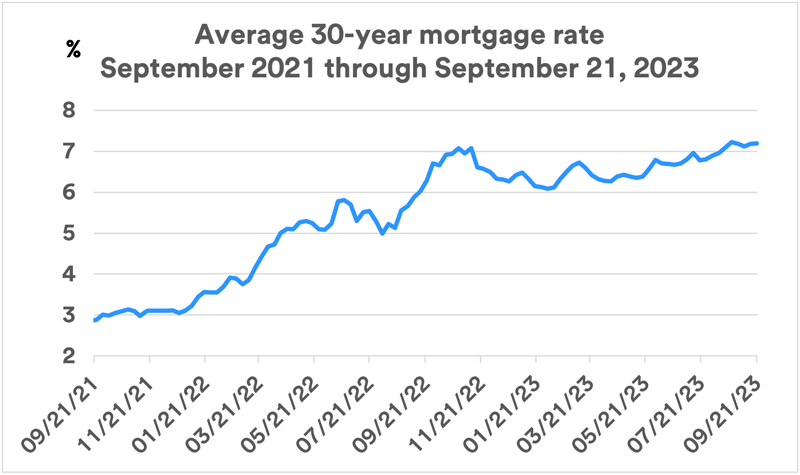

Source: Federal Home Loan Mortgage Corporation (Freddie Mac).

Interest rates soaring to 7.5% has a significant impact on the real estate market, affecting both buyers and sellers in several ways:

Impact on Buyers:

- Reduced Buying Power: Higher interest rates mean higher mortgage payments, reducing what buyers can afford. This might force buyers to look for smaller homes or homes in less desirable locations.

- Lower Demand: The high cost of borrowing could discourage many potential buyers from entering the market, leading to reduced demand.

- Increased Renting: As mortgages become less affordable, renting might become a more attractive option, driving up demand and prices in the rental market.

- Stricter Loan Approval: Banks might tighten lending standards in response to higher rates, meaning buyers would need better credit scores and a higher down payment to qualify for a loan.

Impact on Sellers:

- Lower Prices: Reduced demand could put downward pressure on home prices, making it a buyer’s market.

- Longer Time on Market: Homes might take longer to sell due to the reduced pool of eligible buyers.

- Negotiating Power: Buyers may gain more negotiating power, forcing sellers to make concessions like covering closing costs or making additional improvements to the home to make the sale.

- Cash is King: Cash buyers, not subject to interest rates, may find themselves with increased buying power and leverage in negotiations.

Impact for You:

Our nation’s history average interest rates for 30 year fixed mortgages is 8%. We are currently below that national average.

Forbes Advisor states getting an optimal rate on a home loan can save you a significant amount of money over time. Here are some tips that can help you get the best rate possible for your situation:

- Keep your eye on rates. Mortgage rates are constantly changing. Keeping a close watch will make it easier to find and lock in a better rate.

- Check your credit. When you apply for a mortgage, the lender will review your credit to determine your creditworthiness as well as your interest rate. In general, the higher your credit score, the better your rate will be. To get an idea of where you stand, check your credit before you apply and dispute any errors with the appropriate credit bureau to potentially boost your score.

- Shop around and compare lenders. Consider options from as many mortgage lenders as possible to find the best deal for you. Prospective buyers have saved more than $1,500 over a loan’s term by getting two quotes from lenders and saved roughly $3,000 when they sought five quotes, according to Freddie Mac.

#ourmichiganhome